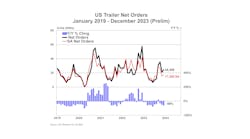

Preliminary net trailer orders decreased “nominally” from February to March, ACT Research reported. At 13,600 units, orders also were lower compared to last March, down 24%. Seasonal adjustment (SA) at this point in the cycle leaves March’s tally essentially unchanged at 13,800 units.

“Against year-ago data still impacted by pent-up demand that is now gone, softer order intake activity continues to meet expectations,” said Jennifer McNealy, director CV market research and publications at ACT Research. “Net orders remain challenged by a backdrop of weak profitability for for-hire truckers. Anecdotal commentary from trailer manufacturers and suppliers through the past several months have indicated this slowing, as they have shared that orders are coming, but at a more tepid pace when compared to the last few years.”

For the trailer industry, weaker fleet revenues are compounded by the power-unit prebuy ahead of the EPA’s implementation of 2027 regulations, which has already begun, McNealy added. As a result, cancellations remain elevated, and decisions about investing limited capex dollars is “swinging the pendulum against trailer purchases right now.”

“While we remain cautiously optimistic and don’t believe this year will be catastrophic for the trailer markets in general, we note that 2024 thus far is matching expectations as a year of transition,” McNealy said. “While some specialty segments have no available build slots until late in 2024 at the earliest, the industry’s largest segments remain under pressure, and cancellations are anticipated to continue their oscillation into and out of elevator territory as dealers and fleets recalibrate their inventory and immediate needs."

Similarly, FTR reported that March trailer orders fell 7,659 from February (-38% from January) to a total of 12,313 units. Orders were down 18% year-over-year and 25% below the average for the last 12 months.

Trailer production, however, increased slightly in March to 23,505 units, while production was down 21% compared to the year before. This build number is “in line” with the average production level seen over the past three years, FTR noted.

“With orders coming in below production levels, backlogs in February fell somewhat, shedding more than 11,500 units to end at more than 151,000 units. The increase in production coupled with the fall in backlogs resulted in some reduction in the backlog-to-build ratio, which stands at 6.4 months,” FTR Chairman Eric Starks said. “This ratio is slightly below the average level for the last half of 2023 but is above the historical average prior to 2020. The current ratio suggests that, overall, trailer manufacturers have little incentive to alter production levels in the near term.”