Though U.S. economic growth remains “tepid” according to analysts, the picture for freight volumes remain positive as a result of supply-and-demand balance within the TL segment, and rate gains should emerge in the second half of the year, experts said.

“We’d already forecasted 5% freight growth for this year in what’s generally considered a lousy GDP [gross domestic product] growth environment, so there is significant upside potential,” Eric Starks, president of research firm FTR Associates, told Fleet Owner.

“A lot of good things are going on,” he added. “The housing market is doing great, especially in terms of existing home sales, and that drives a lot of freight such as furniture, appliances, and home improvement goods. While U.S. manufacturing activity slowed in March, activity is remaining strong, while the annual rate for automotive sales hovers between 15.2 million and 15.4 million; those are good numbers.”

That data reflects a sense of “cautious optimism” within the U.S. business community, noted Sally Buchholz, VP- customer service and marketing for LTL carrier Saia Inc. She pointed to the carrier’s 2013 National Survey of Small-to-Medium Business Executives, which discerned that close to half of the 739 executives participating in its national poll saying the U.S. economy is slightly improving, though only 7% thought it rebounding strongly.

“Small to medium-sized businesses indicate they see some improvement in the economy, but continue to be wary of excess spending or hiring,” Buchholz noted.

Job creation also remains on the upswing, albeit at a slow pace. According to the ADP National Employment Report produced by ADP and Moody’s Analytics, the U.S. private sector added 158,000 in March, with an average gain of 191,000 new private sector jobs per month over the first quarter of 2013.

“Job growth moderated in March [as] construction employment gains paused as the rebuilding surge in the wake of Superstorm Sandy ended,” noted Mark Zandi, chief economist for Moody’s Analytics. “Anticipation of health care reform may also be weighing on employment at companies with close to 50 employees. The job market continues to improve, but in fits and starts.”

Still, the U.S. economy continues to grow albeit slowly in spite of tax hikes, fuel cost increases, and the impact of federal spending cuts, noted John Larkin, a transportation analyst with Wall Street firm Stifel Nicolas in a freight outlook brief – pointing out that while most TL carriers otherwise are not adding capacity, except for those tied to specific dedicated fleet contracts, “supply and demand” is now roughly in balance despite tepid economic growth.

“The most current ISM [Institute for Supply Management] data indicates sustained growth, although perhaps at less than enthusiastic levels,” Larken added. “[Yet] yield momentum continues to favor carriers.”

Stifel projects that TL general contract rates for the first half of 2013 could swing between a 1% drop and a 2% gain year-over-year, with TL general dedicated rates staying flat or growing 2% year-over-year for the first half of 2013. “[But that] could prove to be conservative if the supply/demand equation further tightens,” Larkin said.

Stifel’s LTL rate increase estimates, excluding fuel surcharges, remain at an average of 2.5% year-over-year for 2013, but could be higher depending on TL/LTL industry capacity, freight growth, and carrier capacity/pricing discipline, he noted.

FTR’s Starks told Fleet Owner that one big as-yet unpredictable issue is how inventory restocking plans might impact freight demand for 2013. “A lot of inventory pull-down occurred in the fourth quarter of 2012 and that suggests a pickup in inventory restocking will need to happen at some point,” he said. “From a freight growth perspective, that could be huge.”

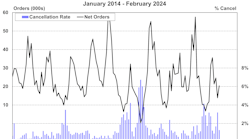

That’s why the 4% decline in net Class 8 truck orders between February and March this year – with March posting an order level of 21,817 units – isn’t upsetting FTR’s freight industry outlook too much as of yet.

“While March orders dipped somewhat from the previous month they were up 11% year over year,” Starks noted. “Combined with January/February orders, that resulted in an annualized rate of 266,080 units for the first three months of 2013.”

Yet because March orders came in above 21,000 units remains a “good sign” for the near-term, he stressed.

“We expect that anything above 19,000 units in orders adds to the backlog of orders to be built which we believe will be confirmed when numbers are finalized mid-month,” Starks noted. “We didn't expect orders to fall from recent levels; however, it is good to see actual data suggesting the market has stabilized with more upside potential for the second half of the year. The next few months’ orders will be critical in understanding the demand pressure as we move into the summer.”

Kenny Vieth, president and senior analyst at ACT Research, echoed those sentiments in his report on Class 5 through 8 net orders – estimated that net Class 8 orders will approach 22,100 units for March, with net Class 5-7 orders hitting roughly 15,200 units.

“While down month over month, March’s Class 8 net orders were up 10% year-over-year and were the fourth best in the past thirteen months,” said Vieth. “For medium duty, the tough year-over-year comparisons mask an otherwise solid order month.”

Jeff Kauffman, a transportation analyst with Sterne Agee, told Fleet Owner that looking at the truck order trend in aggregate for the year rather than on a month-by-month basis indicates that there is growing confidence within the trucking space.

For example, Kauffman pointed out that on a “season-to-date” basis, heavy-duty truck orders are now 10% lower than the prior year, compared to a 16% difference in January and 13% in February.

“When you look at orders collectively, it means we’re closing that truck sales deficit ‘gap,’” he explained. “Remember, too, that 22,000 or so orders [for one month] is still a very respectable number in a slow growing economy.”

Kauffman also pointed out that several other factors could be retarding orders, especially the impact of greenhouse gas (GHG) emission mandates for heavy trucks that go into effect next year.

“Those rules will increase [truck] fuel economy, so if you’re a fleet, you saying to yourself, ‘Why spend money on trucks this year that get 6 mpg on average when we can get trucks that get maybe 8 mpg on average in 2014?’ That’s why fleets will probably just focus on maintenance Cap Ex [capital expenditure] this year just to replace older equipment,” he said.